7 Mistakes You're Making with Inventory Financing (and How to Fix Them)

For e-commerce operators on Shopify or Amazon—and direct sellers running DTC (direct-to-consumer) or social commerce—inventory is your greatest asset and your biggest liability. It is the engine that drives revenue, but it is also a massive sink for your liquid cash. Managing this balance requires more than just good sales, it requires a sophisticated approach to inventory financing.

Many sellers view financing as a last resort or a simple "plug-and-play" solution. This mindset leads to expensive errors that can erode margins and even sink a growing brand. If you want to scale without the constant threat of a stockout, you need to treat your capital strategy with the same rigor as your Facebook ad spend.

Here are the seven most common mistakes e-commerce owners make when seeking working capital for online stores, and how to fix them.

1. Waiting Until You’re in a Cash Crunch to Apply

The worst time to seek funding is when you urgently need it. Businesses under financial pressure are often seen as higher risk, which can lead to fewer options, higher rates, or declined applications.

Be proactive, not reactive. Apply for funding while your business is performing well. Building a relationship with Pure Fast Advance during strong trading periods can give you access to more funding options and faster approvals when opportunities arise. As a business loan broker, we match businesses with suitable lenders based on their needs and circumstances.

When should you apply? Ideally, start the process 30–60 days before placing a major inventory order. This gives you time to compare offers and ensure funds are available when needed.

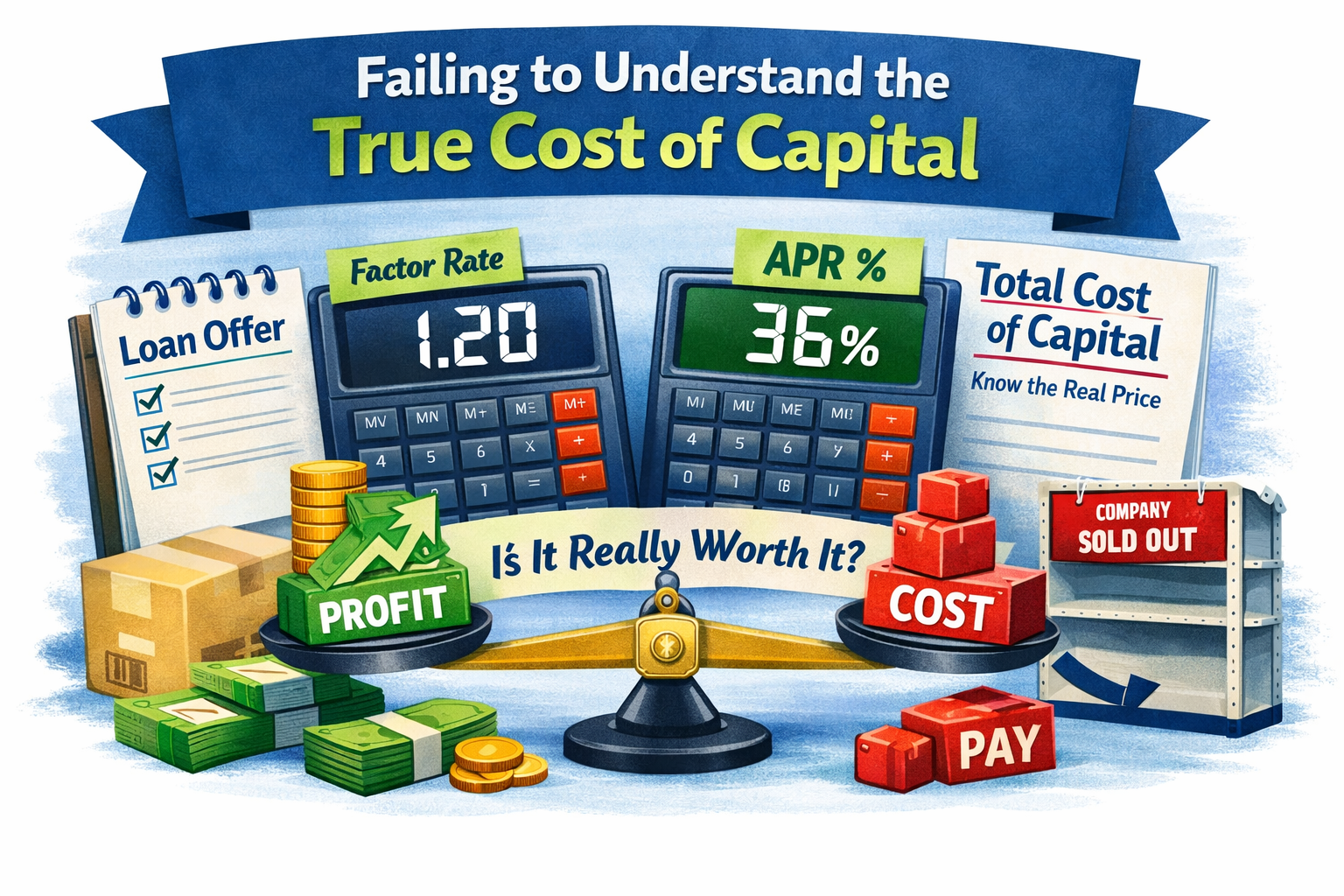

2. Failing to Understand the True Cost of Capital

Many e-commerce owners focus solely on the "monthly payment" without understanding the underlying cost. They often confuse factor rates with annual percentage rates (APR). A factor rate of 1.2 might sound low, but if you have to pay that back in four months, your effective APR is sky-high.

The Fix: Calculate Your ROI on Every Borrowed Dollar

Don't just look at the interest rate. Look at the total cost of the loan versus the profit that inventory will generate. If borrowing £50,000 costs you £5,000 in fees but allows you to generate £30,000 in net profit that you otherwise would have missed, the math works. However, if the financing costs eat 50% of your margin, you are working for the lender, not yourself. Always ask for the "total cost of capital" in plain numbers.

3. Ignoring Seasonal Peaks and Lead Times

E-commerce lives and dies by seasonality. If you are an Amazon seller, your Q4 inventory needs to be manufactured in July and shipped by September. Many sellers wait until October to seek inventory financing, only to realize that by the time the funds hit and the supplier ships, they’ve already missed the peak buying window.

The Fix: Sync Your Funding with Your Supply Chain

Map out your lead times, from the moment you pay the deposit to the moment the goods hit the warehouse. Align your financing to cover these gaps. If you have a 90-day lead time, your working capital needs to be secured 100 days in advance. This prevents the "out-of-stock" death spiral where your organic ranking drops because you couldn't fulfill demand.

What happens if I miss the seasonal window?

Missing a peak season usually results in "dead stock", inventory that arrives too late and must be liquidated at a discount. This creates a double loss: the cost of the loan and the loss of product margin.

4. Over-Borrowing: The "Just in Case" Trap

It is tempting to take every pound a lender offers. However, over-borrowing leads to excess inventory, which carries its own costs, warehousing fees, insurance, and the risk of obsolescence. If you borrow more than you can realistically sell in a single cycle, you are paying interest on capital that is literally sitting on a shelf gathering dust.

The Fix: Borrow Based on Data, Not Optimism

Use your historical sales data to forecast demand. If your sales are growing at 10% month-over-month, don't borrow enough to triple your inventory "just in case." Use inventory financing to cover your 1.5x growth scenario, not a 5x fantasy. Keep your capital lean and your turnover high.

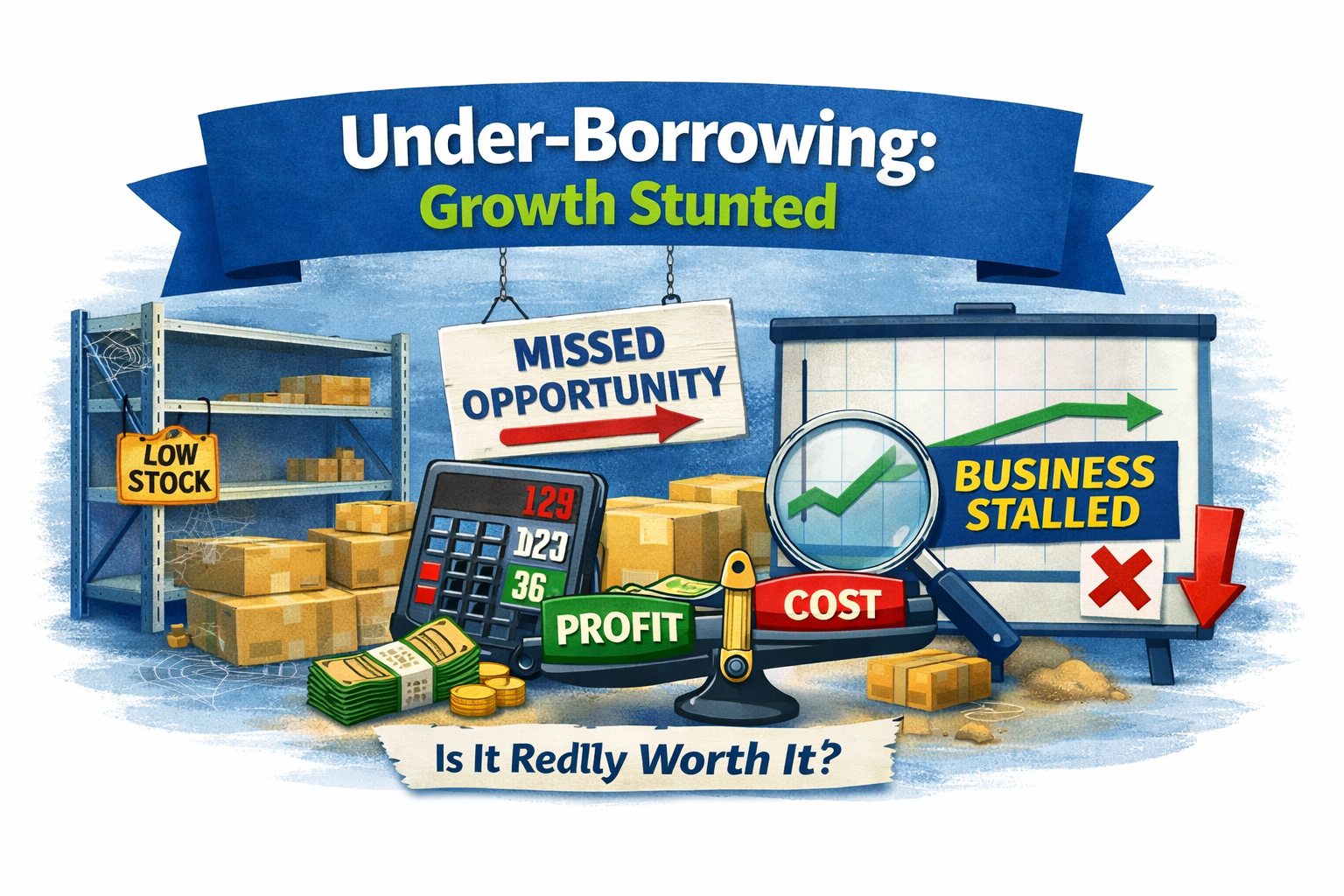

5. Under-Borrowing: The Growth Stunt

The opposite of over-borrowing is being too conservative. If you only borrow enough to maintain your current sales volume, you aren't using e-commerce growth capital for its intended purpose: growth. Under-borrowing leaves you unable to take advantage of bulk-buy discounts from suppliers or handle a sudden surge in demand from a viral marketing campaign.

The Fix: Calculate the "Opportunity Cost" of Not Borrowing

If a supplier offers a 10% discount for ordering 5,000 units instead of 1,000, and the cost of financing that larger order is only 4%, you are losing 6% by not borrowing. Don't be afraid of debt if it is used to secure a clear, higher return.

6. Poor Inventory Tracking and Data Management

Lenders want to see that you know your numbers. If you cannot produce a clean report showing your Days Sales of Inventory (DSI), SKU-level profitability, or return rates, you will struggle to get favorable terms. Many sellers rely on "gut feeling" rather than a dashboard, which is a red flag for any professional firm.

This matters even more with non-standard lenders (often the lenders that can move faster or take a more flexible view than a high-street bank). They often ask for management accounts (your in-year Profit & Loss, balance sheet, and sometimes cash flow)—typically the last 3 to 6 months—so they can see how you’re trading right now, not just what last year looked like.

The Fix: Keep Management Accounts “Funding-Ready” All Year

Instead of scrambling at the last minute:

Update bookkeeping monthly (not quarterly)

Reconcile bank feeds weekly (usually 20–30 minutes if you stay on top of it)

Keep a simple monthly pack: P&L, balance sheet, aged debtors/creditors, and a basic stock report

When you do need funding, you can usually submit clean numbers in 24–48 hours—rather than losing a week pulling things together while stock is running out.

The Fix: Implement Robust Inventory Management Systems

Whether you use Shopify’s native tools or a third-party system like Linnworks or Skubana, ensure your data is clean. Professional lenders, especially those focused on commercial lending, often integrate directly with your store via API. If your data is messy, their algorithm will view you as high-risk.

What metrics do lenders look for most?

Lenders primarily look at your "Inventory Turnover Ratio" (how many times you sell and replace stock in a period) and your "Gross Margin Return on Investment" (GMROI). High turnover and stable margins indicate a healthy business that can easily service debt.

7. Not Shopping for the Right Lender

Taking the first offer that hits your inbox, often a Merchant Cash Advance (MCA) with aggressive daily repayments, is a common mistake. Standard banks often don't understand the "asset-light" nature of e-commerce, while some online lenders charge predatory rates because they know you’re in a rush.

The Fix: Find a Specialist Who Speaks Your Language

You need a partner that understands the nuances of digital marketplaces, Amazon's payout cycles, and Shopify's ecosystem. Look for lenders that offer flexible repayment terms tied to your sales, this protects your cash flow during slower weeks. If a lender doesn't ask about your platform or your lead times, they likely don't understand your business.

Common Questions About E-commerce Inventory Financing

Is inventory financing the same as a traditional bank loan?

No. Traditional bank loans often require physical collateral (like real estate) and years of tax returns. Inventory financing is typically "asset-based," meaning the inventory itself: or your future sales: acts as the security for the capital.

How fast can I get access to working capital?

While traditional banks can take months, specialized e-commerce lenders can often provide funding in 24 to 72 hours, provided your store data is easily accessible for review. Check out our FAQs for more on timelines.

Can I use the funds for things other than inventory?

While "inventory financing" is specifically for stock, many working capital products allow you to use the funds for marketing, hiring, or even acquisition finance if you are looking to buy another brand.

Summary: Practical Takeaways for E-commerce Success

To stop making these mistakes and start using financing to your advantage, follow these steps:

Audit Your Lead Times: Know exactly how long it takes for cash to turn back into stock.

Clean Your Data: Ensure your inventory tracking is accurate before you talk to a lender.

Calculate Total Cost: Stop looking at "monthly payments" and start looking at the total cost of the capital vs. the profit it enables.

Forecast Seasonality: Secure your Q4 and Q1 funding while your Q3 numbers are looking strong.

Keep Management Accounts Updated: Non-standard lenders often want in-year numbers (typically last 3–6 months). Don’t rush them the week you need cash.

Build a Relationship Early: Don’t wait until you’re under pressure. A broker relationship built ahead of time usually means faster placement, cleaner submissions, and better-fit options when you need funding.

Inventory is a game of math and timing. By avoiding these common pitfalls, you ensure that your business has the working capital for online stores required to scale without the constant fear of the "sold out" button appearing at the worst possible time. For more direct advice on securing your next round of funding, visit our home page.